Arushi Jain, The Times of India 8 June 2026 Their faces have launched many campaigns and brought crores to the film industry. But can they sell a moisturiser as successfully? India’s beauty market is the hottest growth story globally, estimated to reach $40 billion from $23 billion (2026) and eyeing the fourth-largest spot by 2030 (currently at number seven). Last month, Estée Lauder announced the buyout of Forest Essentials, one of India’s oldest, Ayurveda-based brands. In 2025, Hindustan Unilever acquired five-year-old skin and hair care brand, Minimalist. A 2025 McKinsey & Company x Business of Fashion survey found that 78%…

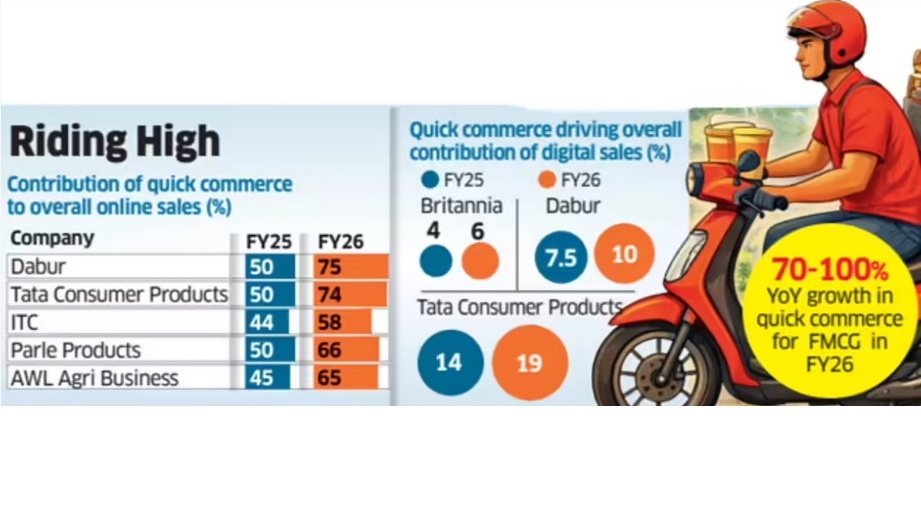

Writankar Mukherjee and Aanya Thakur, Economic Times Kolkata/Mumbai, 27 May 2026 Quick commerce has become the dominant online sales channel for India's top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms. Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment. Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and…

Vaeshnavi Kasthuril, MINT Bengaluru, 25 May 2026 Value fashion retailers across the country are likely to face margin pressure in the upcoming quarters as rising crude oil prices are driving up the cost of polyester and other fabrics. Executives at V-Mart Retail Ltd, Vishal Mega Mart Ltd, and Kewal Kiran Clothing Ltd (KKCL) said crude oil-linked inflation has begun to push up yarn and sourcing costs across apparel and general merchandise categories, with the full impact expected to play out over the next few months. Value fashion retailers face a double whammy: their heavy reliance on polyester and synthetic blends…

The ET Now Swadesh panel discussion focussed on the dual challenge facing the Indian economy: a weakening rupee and rising crude oil prices, which together are driving "imported inflation" and straining household budgets. Devangshu Dutta (Founder, Third Eyesight) put forth the following key points during the discussion (the video link is under the text summary below): 1. Dual Impact on Industry and Consumers: Inflationary pressures are hitting both sides of the market. While industries are facing rising input costs, the decision of how much cost to pass on to the consumer (through price increases or altering packaging sizes) rests with…

Anushka Jha & Kausar Madhyia, Afaqs 12 May 2026 On May 10, Prime Minister Narendra Modi, in his address to the nation, made some appeals to the citizens of India. In addition to asking Indians to re-adopt Covid-like practices of working from home and refraining from travel abroad, the prime minister also appealed to the citizenry to stop buying gold for weddings for a year. The appeals come in response to the global energy crisis and economic instability triggered by the US-Iran war and the consequent West Asia conflict, which makes import-dependent commodities like gold especially vulnerable. The market reaction…

India's consumers have always bought groceries frequently through the week, and quick commerce today is enabling that trend for the digital-native generation.

#QuickCommerce #India #Ecommerce #FMCG #food #consumerbehaviour

The @ETNowSwadesh discussion on the dual challenge of a weakening rupee & rising crude oil prices driving "imported inflation". @devangshu on the panel with @davemansi145 as anchor

As legacy retailers balance speed with customer experience, is near-instant delivery a sustainable goal for fashion, or will the costs outweigh the rewards?

@devangshu

#Retail #SupplyChain #Strategy #India #Fashion #SupplyChain #Omnichannel