Sowmya Ramasubramanian, Vaeshnavi Kasthuril (MINT) Bengaluru, 13 July 2026 India's vertical quick-commerce startups across categories like baby care, medicines and fashion, backed by venture capital heavyweights, are beginning to redefine what “quick” means. For some, the race is no longer about cutting delivery times by a few more minutes. Instead, founders are increasingly talking about better assortment, sharper curation, stronger supply chains and healthier unit economics as the factors that will decide whether the model survives. Baby care platform Ozi, backed by Blume Ventures and RTP Global, has settled on a roughly 60-minute delivery promise. Founder Amit Sah told Mint…

Neethi Lisa Rojan & Vaeshnavi Kasthuril, MINT Mumbai/Bengaluru, 8 July 2026 The collapse of the US-Iran peace deal in less than a month has rattled India's consumer sector, reviving fears that higher oil prices and fresh supply-chain disruptions could squeeze demand just as companies were betting on a broader recovery. The renewed uncertainty followed US President Donald Trump's declaration on Wednesday that the peace deal with Iran was effectively over, alongside Washington's decision to end a sanctions waiver on Iranian energy supplies. The market reaction was swift. The Nifty FMCG Index fell 2.49% on Wednesday, underperforming the broader market as…

Vaeshnavi Kasthuril, MINT 30 June 2026, Mumbai Advent International-backed Modenik Lifestyle Pvt. Ltd is doubling down on its portfolio of legacy innerwear brands, planning to scale each label into a sizeable business rather than rely on a single flagship brand. "Each of the brands must grow big enough to be called a company of its own," Shekhar Tewari, chief executive and executive director, told Mint. The company has four brands: premium women's innerwear label Enamor, value brand Slimz, mass-premium men's label Dixcy Scott, and premium men's innerwear brand Levi's. "These brands are very strong in their respective segments. They complement…

Sharleen D’souza & Shivani Shinde, Business Standard Mumbai, 21 June 2026 Online beauty marketplaces Reliance Retail Ventures’ Tira and Nykaa have a common mantra: growing in-house brands. Successful brand acquisitions and margin growth seem to fuel the push. “With private labels, margins are better. It also helps both companies plug the gap in the market which other brands are not present in,” Devangshu Dutta, chief executive officer (CEO) of Third Eyesight, told Business Standard. Within in-house brands, products need some investment in research and development (R&D), he explained. Harish Bijoor, brand and business strategy consultant at Harish Bijoor Consults, said…

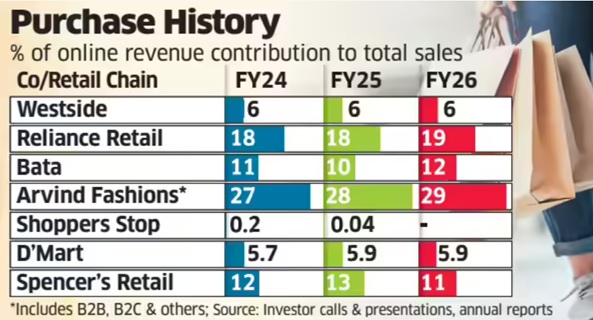

Aanya Thakur & Writankar Mukherjee, Economic Times 12 June 2026, Mumbai/Kolkata India's leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing. An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer's Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive…

Geopolitical friction has again sparked renewed concerns over inflation and rising input costs for FMCG companies as @itmeansjustice @whysnavi write. @devangshu commented.